Buying a Residential Property in Singapore

Our local residential market has finally picked up after a few years of sluggish growth. The increase in transaction volume and upswing in prices are fueled by an increasing number of successful collective sales and record high bid prices under the government land sales program. Buyers and investors who were sitting on the fence and undecided in the past have also entered the market as they hope to ride on the price uptrend. Packed show flats during weekends are a regular sight again as developers step up on their new launches.

With the bright and positive sentiments in our local residential market, it will be worthwhile to relook into some of the key considerations when buying a residential property before one gets carried away by the euphoria.

Understand your Needs and Objectives

In an upbeat market where volume and prices are increasing on a monthly basis, consumers tend to rush into making decisions with the fear of missing out on a piece of the pie. In some instances, these behaviours may result in consumers ending up with a wrong product i.e. mismatch in their expectations or objectives with the actual product. It is therefore crucial to examine one’s needs and objectives before committing to a purchase.

A development in an accessible location with full-fledged facilities, spacious layout and bigger unit size will tend to suit the needs of a growing family with young kids whereas a unit which is smaller in size but located near tenant catchment areas such as the Central Business District (CBD) may be a good investment option for rental income.

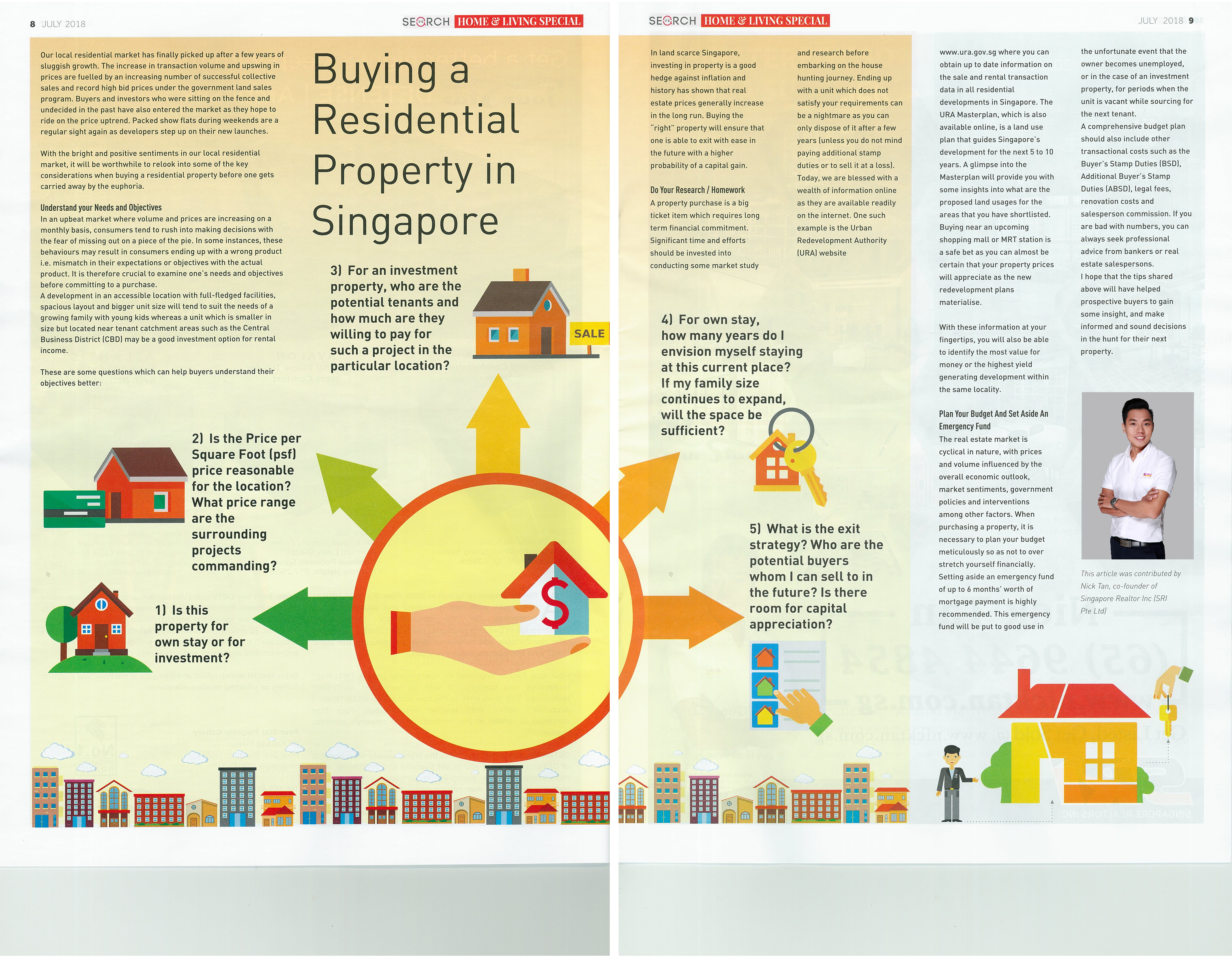

These are some questions which can help buyers understand their objectives better:

- Is this property for own stay or for investment?

- Is the Price per Square Foot (psf) price reasonable for the location? What price range are the surrounding projects commanding?

- For an investment property, who are the potential tenants and how much are they willing to pay for such a project in the particular location?

- For own stay, how many years do I envision myself staying at this current place? If my family size continues to expand, will the space be sufficient?

- What is the exit strategy? Who are the potential buyers whom I can sell to in the future? Is there room for capital appreciation?

In land scarce Singapore, investing in property is a good hedge against inflation and history has shown that real estate prices generally increase in the long run. Buying the “right” property will ensure that one is able to exit with ease in the future with a higher probability of a capital gain.

Do Your Research / Homework

A property purchase is a big ticket item which requires long term financial commitment. Significant time and efforts should be invested into conducting some market study and research before embarking on the house hunting journey. Ending up with a unit which does not satisfy your requirements can be a nightmare as you can only dispose of it after a few years (unless you do not mind paying additional stamp duties or to sell it at a loss). Today, we are blessed with a wealth of information online as they are available readily on the internet. One such example is the Urban Redevelopment Authority (URA) website www.ura.gov.sg where you can obtain up to date information on the sale and rental transaction data in all residential developments in Singapore. The URA Masterplan, which is also available online, is a land use plan that guides Singapore’s development for the next 5 to 10 years. A glimpse into the Masterplan will provide you with some insights into what are the proposed land usages for the areas that you have shortlisted. Buying near an upcoming shopping mall or MRT station is a safe bet as you can almost be certain that your property prices will appreciate as the new redevelopment plans materialise.

With these information at your fingertips, you will also be able to identify the most value for money or the highest yield generating development within the same locality.

Plan your Budget and set aside an Emergency Fund

The real estate market is cyclical in nature, with prices and volume influenced by the overall economic outlook, market sentiments, government policies and interventions among other factors. When purchasing a property, it is necessary to plan your budget meticulously so as not to over stretch yourself financially. Setting aside an emergency fund of up to 6 months’ worth of mortgage payment is highly recommended. This emergency fund will be put to good use in the unfortunate event that the owner becomes unemployed, or in the case of an investment property, for periods when the unit is vacant while sourcing for the next tenant.

A comprehensive budget plan should also include other transactional costs such as the Buyer’s Stamp Duties (BSD), Additional Buyer’s Stamp Duties (ABSD), legal fees, renovation costs and salesperson commission. If you are bad with numbers, you can always seek professional advice from bankers or real estate salespersons.

I hope that the tips shared above will have helped prospective buyers to gain some insight, and make informed and sound decisions in the hunt for their next property.